THE year 2021 began well for the stock market, as investors were betting on a global economic recovery. Commodity prices were also surging to new highs.

But emerging markets took a hit when Covid-19 cases led by the Delta variant began rising. Another headwind came in the form of China’s regulatory clampdown on its technology, education and property sectors.

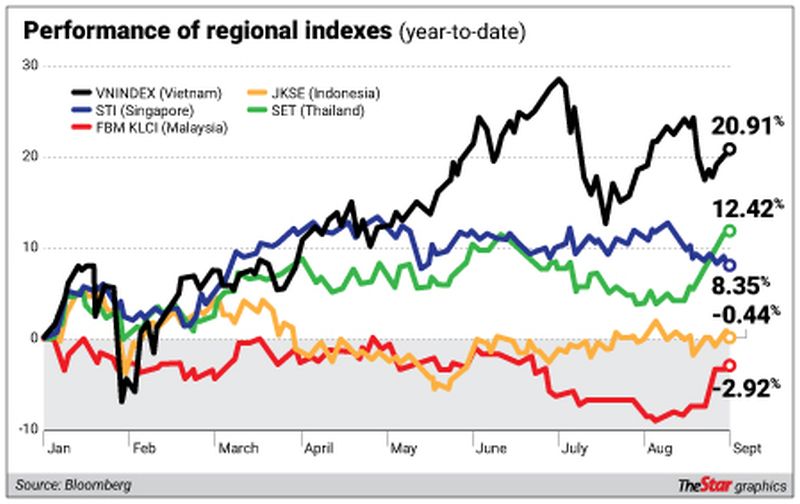

As a result, the Malaysian stock market has been one of the worst performers in the region. The MSCI Emerging Market Index slipped by 1.6% in the first half of this year. In contrast, many major markets, especially the United States, surged significantly.

Since last year, foreign investors have been dumping Malaysian equities. In 2020, the local market saw net selling of RM24bil while another RM5.9bil of foreign holdings left the local market in the first half of this year, according to data by MIDF Research.

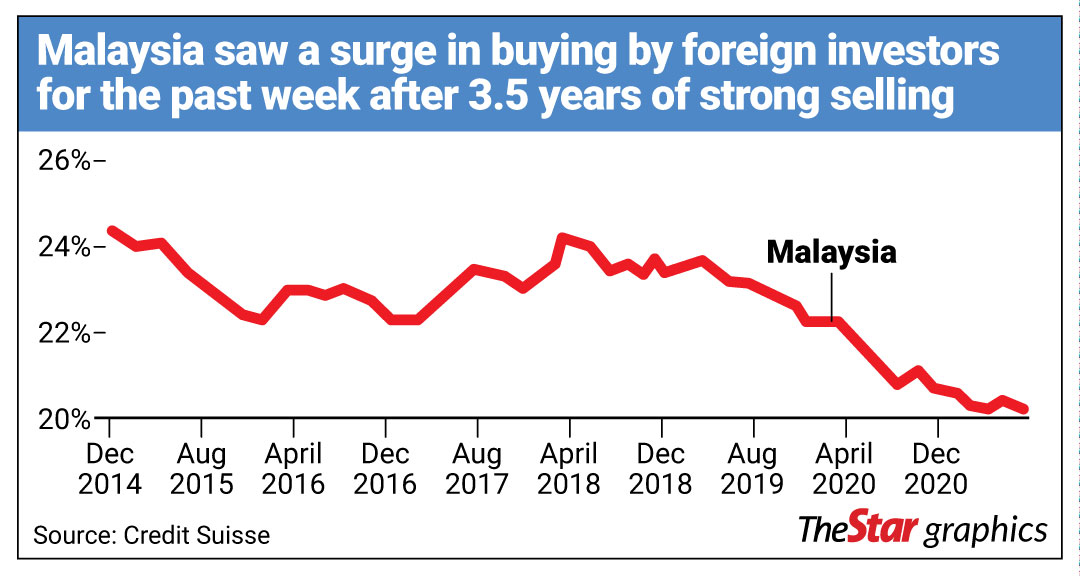

However, the trend seems to be reversing. Last week, the local stock market received a much-needed boost after foreign investors bought almost RM1bil worth of equities.

“There are signs the selldown has ended. Malaysia saw a surge in buying over the last week after three and half years of strong selling,” points out a recent report by Credit Suisse.

The local benchmark index, the FBM KLCI, which fell as much as 5.7% this year, managed to recover half of its losses over the last two weeks. This was driven by investors and fund managers who are of the view that uncertainties of economic growth have been reduced due to the country’s aggressive vaccination programme.

“There are also reduced political uncertainties and Malaysia looks attractive when compared with the stretched valuations in other markets,” says one fund manager.

The upcoming 12th Malaysia Plan and Budget 2022 are likely to provide more clarity and pave the way for further economic growth.

Should this performance sustain, the Malaysian market could chart a positive rebound by the end of this year.

Areca Capital Sdn Bhd executive director and chief executive officer Danny Wong Teck Meng expects local stocks to do better in the medium to long term.

“The market is re-pricing those factors now. Over the past two to three months, the market had been trending down due to the double whammy of Covid-19 and politics,” he says.

He adds that investors should be selective as some sectors are still affected by the pandemic.

“Prices of equities are driven by a combination of liquidity flows, risk appetite and ultimately, the intrinsic value of the underlying assets.

“So, pandemic or not, our philosophy has remained the same,” he says.

“We look into factors such as long-term trends, valuation, liquidity and management quality,” he adds.

It is worth noting that daily new Covid-19 cases in Malaysia are still hovering around the 20,000-mark, despite most part of the country being in a lockdown for more than two months.

Bank Islam chief economist Mohd Afzanizam Abdul Rashid says while he expects the economy to accelerate from the fourth quarter of 2021 onward, the high Covid-19 numbers and the prolonged lockdown pose risks for a smooth recovery.

“The jobless rate is still high. Small and micro small and medium enterprises are still facing operational constraints, which could drain their cashflows.

“The longer the movement control order, the more harm it will do to the economy. So the situation is highly fluid and warrants active intervention by the government,” he says.

He points out that as long as there are standard operating procedures to be observed, businesses will continue to operate at a higher cost. He also predicts cautious consumer spending in the next two to three years.

“Businesses will continue to be mindful of their hiring pace in order to keep their overhead costs and margins at reasonable levels,” Mohd Afzanizam says.

Oversold and attractive valuation

However, some reckon that Malaysian stocks are attractive due to the discounts at which they are trading, plus the fact that all bad news have been priced in.

“Our market looks attractive now. It has been oversold over the past few months. However, we expected some volatility as economic activity in the country is opening up in stages,” says Rakuten Trade Sdn Bhd head of equity sales, Vincent Lau.

He says investors should look beyond the third quarter when sectors such as construction, property and tourism would do better as domestic demand recovers.

Lau also likes the banking sector due to its undemanding valuations and lower impact of the current loan moratorium that started in July compared with the blanket moratorium that was imposed last year.

He expects the technology sector to continue doing well due to factors such as 5G rollout, the continuing trend of working from home and as more companies move their businesses online.

An investment banker points out that although the local stock market was muted in the first half of the year, liquidity has remained healthy.

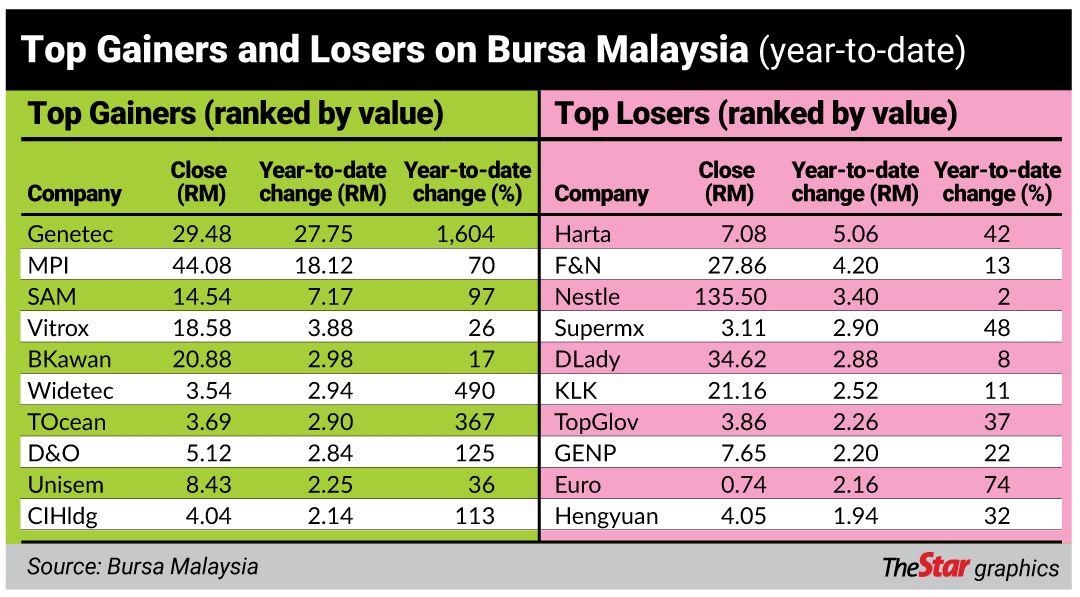

“Many companies, especially those in the technology sector, have embarked on fundraising exercises through private placements. Initial public offerings (IPOs) such as CTOS Digital Bhd and Pekat Group Bhd enjoyed significant oversubscriptions for their shares.”

He says there is still a relatively healthy pipeline of IPOs in Malaysia.

Credit Suisse has upgraded Malaysia and the Philippines to “overweight” recommendations in its Asia-Pacific equity research.

It has ranked Malaysia and the Philippines number one and four, respectively, on its Asia-Pacific valuations scorecard. Both countries are also rated as having the second and third-fastest earnings per share (EPS) growth projected for 2020-2022.

“Our optimism on Malaysia and the Philippines rests on attractive valuations, our expectation that infections can fall faster than expected, low foreign weightings and strong EPS recoveries. We think that both are better positioned to withstand the US monetary tightening than in 2013,“ it said in a report on Thursday.

“We like Malaysia for its rapid vaccine rollout, and favour the Philippines for its strong structural growth. We believe that investors have fully discounted Malaysia’s political uncertainties,” it concurs.

US market concerns and inflation risk

Inflation has been one of the risks cited in recent times as there have been fears of it creeping up to dangerous levels due in large to surging commodity prices and excess liquidity in markets. When inflation is too high, it is not good for the economy and individuals because it reduces spending power.

The consumer price index (CPI) in the United States surged to 5.4% in July, the largest since 2008.

While the US Federal Reserve (Fed) has been keeping a close eye on inflation, mulling a cut to its bond-buying programme or lifting its near-zero interest rates, its chairman Jerome Powell has taken the view that inflation is transitory and that prices won’t continue to increase at their current pace for too long.

Juwai IQI global chief economist Shan Saeed foresees that the Fed won’t be able to tighten its monetary policy for at least the next two years as the economy won’t be able to absorb higher interest rates.

He adds that an inflation spike is unlikely.

“The Fed’s minutes didn’t point to any imminent rate hike.

“However, the global markets reacted negatively last week as the Fed could start to tighten its monetary policy and taper its asset purchases at year-end.

“I don’t foresee that will happen. The Fed has been behind the curve in terms of monetary policy outlook which has created risks in the financial markets. There are four risks to be considered when it comes to the market – systematic risk, sovereign bonds, liquidity and valuations,” he says.

He expects inflation to remain subdued in emerging markets due to effective monetary policy used by central banks.

“Malaysia’s central bank has played its cards intelligently to keep structural stability in the market.

“Bank Negara has made tactical and strategic manoeuvring in its policy, which has paid off well and kept the ringgit stable,” Shan says.

He expects the ringgit to remain stable against the US dollar at 3.67 to 4.10 due to high oil prices, solid export and trade growth, domestic demand picking up and a goal of getting 80% of the adult population vaccinated by October.

Nevertheless, the rise in Covid-19 cases globally due to new variants, expectations of monetary policy tightening by the Fed and the continuous rise in stock prices on Wall Street have raised speculation that a correction is due in the market.

Despite the fears, the Dow Jones Industrial Average, S&P 500 and Nasdaq booked fresh records yesterday.

But Rakuten’s Lau foresees a possible pullback in the US markets due to its continuous uptrend and lofty valuations. “I would suggest investors hold some cash to take advantage of any correction in the markets,” he says.

Penjana Kapital chief investment officer Taufiq Iskandar Jamingan says the valuation of the US market will remain supported at least in the short term and that the Fed is likely to keep interest rates low at least because of higher savings.

“There are more savings sloshing around, exacerbated by rising income inequality.

A larger slice of national income is going to the top decile of earners, and these wealthy few tend to save much of this income rather than spend it and this directly pushes rates down.

“If those savings are invested, it would drive up asset prices further and yields would go down,” he says.

While some may view US stocks to be overvalued, Taufiq says many investors are still attracted to technology, healthcare and communication stocks that have become leading sectors since the Covid-19 pandemic hit.

Taufiq says many emerging markets are in a better position today on the back of strong currency reserves and well-managed budgetary and external balances. Many of the region’s large-cap companies also have strong cash buffers.

“The likelihood of a large shock in the form of a reversal of capital flows has also diminished,” he says.

“The clear and frequent communication from the Fed has guided the market that the unwinding of its quantitative easing programme will not be mixed up with expectations that interest rates will rise faster than they should be.

“Substantial economic recovery is needed before that is to happen,” Taufiq says.

The road ahead for Bursa Malaysia looks challenging, especially with economic recovery continuing to be haunted by the uncertainties posed by the pandemic.

Already a subscriber? Log in

Get 20% OFF The Star Digital Access

Cancel anytime. Ad-free. Unlimited access with perks.